Select how you’d like to proceed with your insurance needs.

Schedule a Call Today

Talk to a real insurance expert on your time.

BOOK A CONSULTATION

WHAT’S IN THIS STEP

15-minutes consultation with licensed advisors

Perfect if you’re unsure about coverage needs

Get personalised recommendations

Make upcover your insurance broker

Already have coverage? Let’s simplify your service

CHANGE BROKER

WHAT’S IN THIS STEP

Keep your current carriers & policies

Simple digital authorisation process

Seamless transition to better service

Cyber Insurance

What Is Cyber Insurance? Australia Small Business Guide for 2026

June 15, 2026

12 Mins Read

Cyber insurance is a policy that may help cover financial loss when a cyber incident hits your business. It pays toward legal costs, data recovery, business interruption, ransom support, and third-party claims, subject to policy terms.

This guide explains what cyber insurance covers, what it does not, how much it costs in Australia, real claim examples, and how to qualify for cover in 2026. Plain English. No filler.

At a Glance

Cyber insurance helps Australian businesses recover from cyber events like ransomware, business email compromise (BEC), data breaches, and phishing-led fraud, subject to policy terms.

"Cyber liability insurance", "cyber security insurance", "cyber crime insurance", and "cyber attack insurance" describe the same product. The wording changes; the cover does not.

Global insurer claims data indicates that business email compromise and funds transfer fraud account for a majority of cyber insurance claims by volume, ahead of ransomware (Coalition 2025 Cyber Claims Report). Australian SMEs face similar exposure.

Cyber insurance for an Australian small business typically costs $400 to $7,500 per year, depending on industry, revenue, data sensitivity, and the security controls in place.

upcover arranges cyber insurance for Australian businesses with instant online quotes and a Certificate of Currency issued on policy confirmation.

What Is Cyber Insurance?

Cyber insurance is a specialty business insurance product. It responds to financial loss when a cyber event affects your business, your data, or your customers' data. The policy may pay toward legal defence, recovery costs, customer notification, public relations support, and third-party compensation, subject to the terms of the individual policy.

Several names refer to this same product. In Australian and international insurance markets you may see it called cyber liability insurance, cyber security insurance, cyber crime insurance, cyber attack insurance, cyber risk insurance, or cyber and privacy liability insurance. These terms are largely interchangeable in Australia, although there are subtle differences in scope depending on the insurer. The clearest way to compare policies is by what each section actually covers, not by the marketing name on the cover sheet.

Difference Between First-Party vs Third-Party Cyber Cover

Before anything else, here is the core distinction every business owner needs to understand. Cyber insurance covers two different categories of loss. First-party cover pays for damage to your own business. Third-party cover pays for damage to others caused by an incident at your business.

First-Party vs Third-Party Cyber Cover

First-party cyber cover

Third-party cyber cover

What it pays for

Damage to your own business

Damage to others caused by an incident at your business

Common claim types

Data recovery, business interruption, ransom support, forensic investigation, customer notification

Customer compensation, legal defence, regulatory defence, media liability

Who suffers the loss first

Your business

Your customers, suppliers, or third parties

Typical claim trigger

Ransomware, malware, system outage, internal data exposure

Customer lawsuit, regulator investigation, partner financial loss

Usually included in modern AU policies

Yes

Yes

Most modern cyber policies in Australia include both. Lower-cost or entry-level policies sometimes include only third-party cover. Always read the Product Disclosure Statement before purchase to confirm the scope of cover.

Why Australian Businesses Need Cyber Insurance in 2026

Cyber risk has moved from a fringe concern to a top operational risk for Australian businesses. Three forces are driving this shift in 2026.

The threat landscape has changed: Cyber criminals now target businesses of every size. Global and Australian claims data from 2025 shows that initial ransom demands rose significantly year-on-year. BEC and funds transfer fraud are now the most common cyber insurance claim type by volume globally, while ransomware remains the most expensive single claim category in Australia, responsible for 62 percent of all claim costs (Emergence Insurance Cyber Claims Report 2025). The shift toward email-based fraud means cyber risk is no longer just a technology problem. It is a finance and process problem. For more on this shift, see our guide to cyber insurance claims in Australia.

Major Australian breaches have raised the bar: The Medibank Private breach exposed personal records of 9.7 million Australians. The Optus breach affected approximately 9.8 million customers. The Latitude Financial incident involved around 14 million records. These events have reshaped insurer expectations, regulatory scrutiny, and customer notification practices across the country, and have made cyber insurance a routine question in customer onboarding and supplier due diligence.

Privacy law has tightened: The maximum penalties for serious privacy interferences were substantially increased in 2022. The Privacy and Other Legislation Amendment Act 2024 introduced further privacy reforms, including new lower-tier civil penalties and a statutory tort for serious invasions of privacy, which commenced on 10 June 2025. The Office of the Australian Information Commissioner (OAIC) administers the Notifiable Data Breaches (NDB) Scheme, which requires eligible breaches to be notified to the OAIC and to affected individuals.

For most businesses, the combined cost of legal review, customer notification, regulatory defence, and customer remediation after a single incident often exceeds the cost of an annual cyber insurance premium.

What Does Cyber Insurance Cover?

A cyber insurance policy is built from separate insuring sections. Each addresses a different category of loss. The sections below explain what most Australian cyber policies include in 2026.

First-party costs (your direct losses): First-party cover responds to the direct financial impact a cyber incident has on your own business. It commonly includes forensic investigation to identify the cause and scope of the incident, data recovery and restoration of systems and lost information, and business interruption losses from system downtime.

Many policies also cover cyber extortion costs (which may include ransom support, subject to policy wording and applicable law), crisis management and public relations support, and customer notification costs in line with NDB Scheme obligations. Additional first-party cover often includes credit monitoring services for affected individuals where required, and hardware replacement where systems are permanently damaged by malware. Sub-limits and conditions vary by insurer, so the policy schedule is the source of truth on what is and is not included.

Third-party costs (claims against you): Third-party cover responds when others suffer loss because of a cyber incident at your business. It commonly includes legal defence costs for civil claims related to a cyber incident, compensation payable to affected customers, suppliers, or partners, and regulatory defence costs in OAIC or other regulatory investigations. Some policies may also cover indemnifiable fines and penalties where applicable law permits, and media liability claims for content published as part of the incident.

Note: if the regulatory investigation relates to a data breach under the Privacy Act, your cyber policy covers the investigation response costs. However, a separate management liability insurance policy may also respond to statutory liability for regulatory defence costs, depending on how the investigation is classified. The two policies complement each other.

Incident response support: Many cyber policies in Australia include access to an incident response team on 24/7 standby. This typically includes a breach coach, legal counsel, IT forensics specialists, and PR support. For a business with no in-house cyber expertise, this access alone can determine how an incident plays out. Cover is subject to the terms of the individual policy.

What cyber insurance typically does not cover: Exclusions matter as much as inclusions. The most common cyber policy exclusions in 2026 include costs to upgrade or improve security after an incident (some policies include limited "betterment" cover), theft of physical hardware not linked to a cyber event, loss of future profits or speculative reputational harm, losses caused by failure to maintain stated security controls, acts of war or state-sponsored cyber events (depending on policy wording), and prior known incidents or undisclosed vulnerabilities at the time the policy is taken out.

Critically, Australian industry data suggests that around 40 percent of cyber insurance claims faced disputes or denial in the past year, most commonly because the business failed to maintain the security controls it declared at application. The most frequent reasons include lapsed multi-factor authentication, unpatched systems, and undocumented changes to the IT environment after the policy was issued.

Always read the Product Disclosure Statement, policy wording, and Target Market Determination before purchase.

The Most Common Cyber Threats Facing Australian Businesses

The shape of cyber risk has changed. Ransomware still gets the headlines, but the most common claim event in Australia today is business email compromise. Below are the five threat types Australian small businesses face most often.

Business email compromise (BEC). BEC is where a criminal compromises or impersonates a business email account. The most common variant in 2026 involves a fake invoice or a request to update supplier bank details. Funds are transferred to the criminal's account and are rarely recovered. Global insurer claims data indicates that BEC and funds transfer fraud together account for the majority of cyber insurance claims by volume. Australian SMEs face similar exposure, but claim frequency varies by insurer, industry, and policy wordings. BEC affects every industry, from accountants handling client funds to real estate agents managing settlement payments to tradies using digital invoicing tools.

Ransomware. Ransomware is malicious software that encrypts the business's systems. The criminal demands payment for the decryption key, often alongside threats to publish stolen data. Ransomware remains the most expensive cyber claim category. The average cost of a ransomware incident for Australian SMEs nearly doubled from $106,500 in 2021 to $207,600 in 2024 (Emergence Insurance Cyber Claims Report 2025). Many policies may cover ransom payments and related extortion costs, subject to policy wording and applicable law. The decision to pay is complex and policies typically require insurer consent and a regulatory review before any payment. Paying a ransom to a sanctioned entity may breach Australian financial sanctions law regardless of insurance coverage.

Phishing. Phishing describes fraudulent emails or messages designed to trick someone into clicking a malicious link, opening an infected attachment, or sharing login credentials. Phishing is the entry point for most ransomware and BEC attacks. Training staff to recognise phishing is one of the highest-impact controls a business can implement.

Data breach. A data breach is unauthorised access to or theft of business or customer data. Eligible breaches must be notified to the OAIC and affected individuals under the NDB Scheme. Even unintentional data exposure can trigger a notification obligation if personal information is at risk of serious harm.

Supply chain attack. A supply chain attack is a compromise of a third-party service provider that affects the business through trust relationships. The 2023 HWL Ebsworth incident is a notable Australian example, where downstream clients were affected by the breach of a single law firm. For more real-world examples, see our guide to cybercrime examples in Australia.

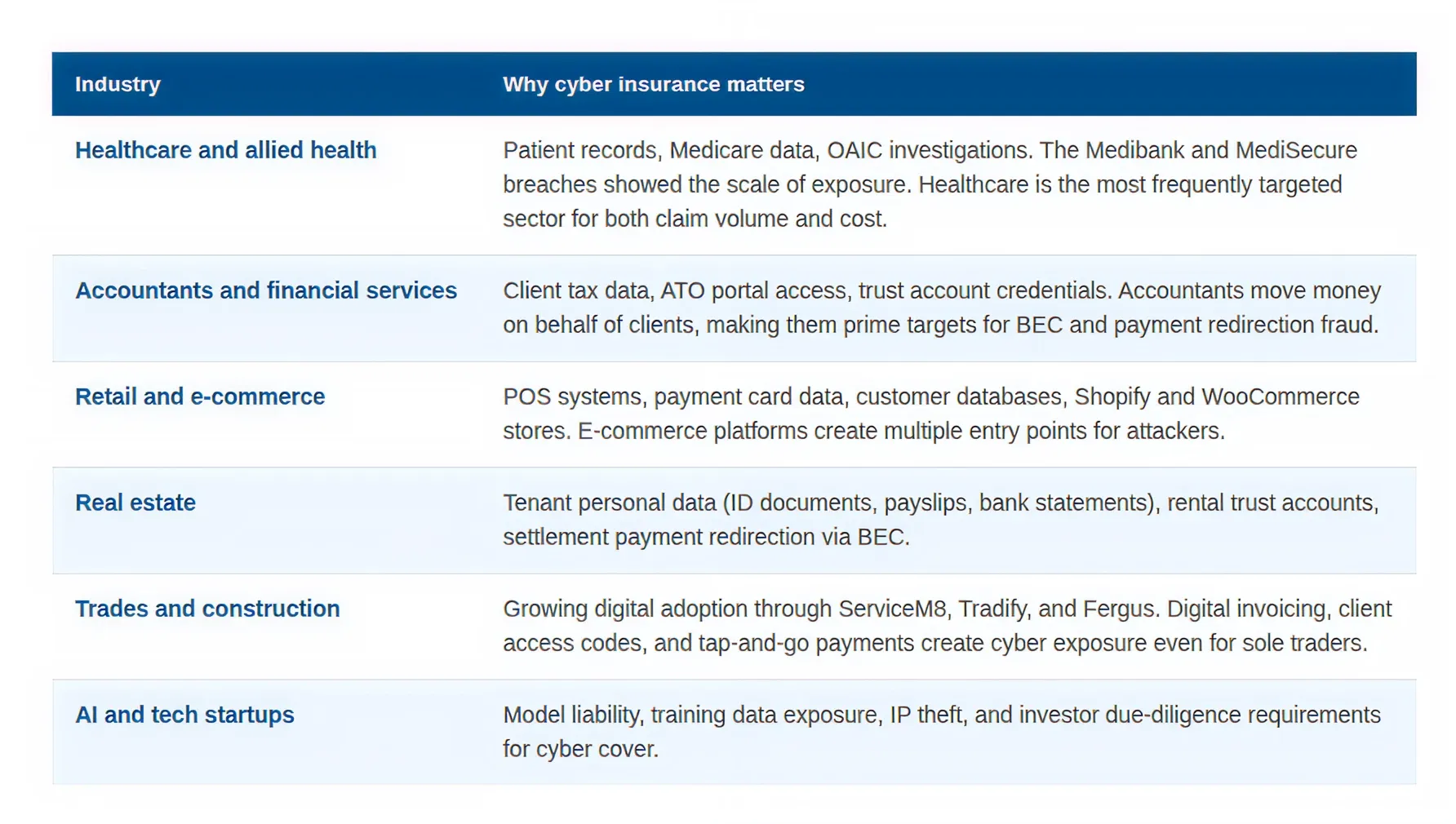

Cyber Insurance by Industry

Cyber risk looks different depending on what your business does and what data you handle. Some industries face specific threats that make cyber insurance not just important but often a contractual or regulatory requirement.

If your industry is not listed, the general rule is: if your business stores customer data, processes payments, or relies on digital systems, you have cyber exposure. upcover arranges cyber insurance across multiple businesses & industries.

How Much Does Cyber Insurance Cost in Australia?

Premiums vary based on industry, revenue, claims history, data sensitivity, and the security controls in place. The table below shows indicative ranges for typical Australian businesses in 2026.

Cost ranges are indicative, based on 2026 Australian commercial cyber insurance market data. Your actual premium depends on your specific business circumstances.

The biggest single driver of premium is the industry sector and the sensitivity of the data your business handles, followed by annual revenue and the number of records held. Businesses with mature security controls, particularly multi-factor authentication (MFA) and regularly tested backups, generally attract lower premiums. Industry data indicates that documented controls aligned with the ASD Essential Eight framework can reduce premiums materially compared to equivalent businesses with no documented security programme. The reduction varies by insurer and risk profile.

Business insurance premiums are typically deductible as a business operating expense under section 8-1 of the Income Tax Assessment Act 1997.

Real-World Cyber Claim Scenarios

The scenarios below illustrate how a cyber insurance policy may respond. Outcomes in real claims depend on the facts of the matter and the terms of the individual policy.

Scenario 1: Business email compromise. An accounts payable officer at a 12-person engineering firm receives an email that appears to be from a trusted supplier. The email asks the firm to update the supplier's bank details before an upcoming $85,000 invoice. The change is approved and the funds are transferred. The real supplier follows up two weeks later. Cyber insurance may help cover the funds transfer loss, forensic investigation, and legal advice, subject to policy terms.

Scenario 2: Ransomware attack on a retailer. A retail business with five stores is hit with ransomware after an employee opens a malicious email attachment. All point-of-sale systems are encrypted. The business shuts down for four days while forensics, recovery, and restoration take place. Direct response costs reach $40,000. Lost trading income reaches $120,000. Cyber insurance may help cover both, subject to policy terms.

Scenario 3: Data breach at a health practice. A small allied health practice discovers that an old employee account was used to access patient records months after the employee left. Approximately 600 patient records may have been viewed. The practice retains a breach coach, notifies affected patients in line with the NDB Scheme, and engages legal counsel for the OAIC notification. Total response cost reaches $25,000. Cyber insurance may help cover legal, notification, and credit monitoring costs, subject to policy terms.

Illustrative scenarios only. Coverage depends entirely on the terms of the individual policy.

How to Qualify for Cyber Insurance in 2026

Choosing the right policy is two questions in one. First, will an insurer cover your business? Second, which policy gives you the right protection?

What insurers look for during underwriting. Cyber insurers in 2026 underwrite specific security controls. The most common minimum requirements are multi-factor authentication (MFA) on email, remote access, and privileged accounts; regular, tested data backups stored separately from main business systems; up-to-date software patching across operating systems and key applications; endpoint protection on all business devices; a documented incident response plan; and annual cyber security awareness training for all staff.

Businesses without these controls may be declined cover or quoted at a significantly higher premium. Building these controls before applying generally lowers both the premium and the chance of a claim. The Australian Cyber Security Centre publishes the Essential Eight maturity model at cyber.gov.au, which most Australian insurers reference informally during underwriting.

What to look for when comparing policies. When comparing cyber insurance policies, the cover limit and any sub-limits on specific sections such as ransomware, BEC, or social engineering are the first thing to check. The retroactive date in the policy, which determines how far back the cover reaches, is the second. From there, look at whether 24/7 incident response support is included or charged separately, whether the policy covers funds transfer fraud and social engineering distinctly from BEC, and the scope of notification and regulatory defence cover for the OAIC and other regulators. Finally, read the exclusions list carefully, paying particular attention to the wording of any war and state-sponsored attack exclusion.

upcover is a digital-first insurance broker helping Australian businesses arrange the right insurance without paperwork or phone queues. upcover arranges cyber insurance across sole traders, small businesses, mid-market companies, and tech startups, with instant online quotes for eligible businesses and a Certificate of Currency issued on policy confirmation.

Backed by access to 80+ Australian and global insurance partners, upcover has helped more than 70,000 Australian businesses arrange cover and holds a 4.9/5 customer rating. Cover is tailored to the business type, from sole traders through to growing technology operations.

Monthly pay-as-you-go direct debit options.

Instant Certificate of Currency on policy confirmation.

70,000+ businesses covered across Australia.

upcover Pty Ltd ABN 17 628 197 437 is a Corporate Authorised Representative (CAR 1299211) of Experience Insurance Services Pty Ltd ABN 41 657 596 506, AFSL 539078.

FAQ

What is cyber insurance?

Cyber insurance is a specialty business insurance product that responds to financial loss following a cyber incident. It may help cover legal defence, data recovery, business interruption, ransom support, customer notification, and third-party claims, subject to the terms of the individual policy. It is built for businesses that hold customer data or rely on digital systems.

Is cyber liability insurance the same as cyber insurance?

In Australia, yes. "Cyber liability insurance", "cyber security insurance", "cyber crime insurance", and "cyber attack insurance" all describe the same broad product. Subtle differences in scope exist between insurers, but the underlying cover is the same: protection against financial loss from cyber events. Always check the Product Disclosure Statement for the specific cover offered.

Do small businesses really need cyber insurance?

Most Australian small businesses today face real cyber exposure. Even a single business email compromise can cost tens of thousands of dollars in unrecovered funds and legal review. Notifiable Data Breach Scheme obligations, customer notification costs, and OAIC scrutiny add further expense after an incident. For most small businesses, the annual premium is a fraction of a single incident's total cost.

How much does cyber insurance cost in Australia in 2026?

Indicative ranges in 2026 are $400 to $900 per year for a low-exposure sole trader, $700 to $2,500 for a micro business, $2,000 to $7,500 for a small business with up to 20 staff, and $5,000 to $25,000 for a mid-size business. Industries handling sensitive data attract higher premiums. Businesses with documented security controls (MFA, tested backups, incident response plan) may attract lower premiums. The reduction varies by insurer and risk profile.

What does cyber insurance NOT cover?

Cyber insurance typically does not cover costs to upgrade security after the incident, theft of physical hardware unrelated to a cyber event, loss of future profits, losses caused by failure to maintain agreed security controls, acts of war or state-sponsored attacks (depending on wording), and prior known incidents undisclosed at the time the policy was taken out.

Does cyber insurance cover ransomware payments?

Many policies may cover ransom payments and related extortion costs, subject to policy wording and applicable law. The decision to pay is complex and policies typically require insurer consent and a regulatory review before any payment. Paying a ransom to a sanctioned entity may breach Australian financial sanctions law regardless of insurance coverage. Specific cover may depend on the facts of the incident and any sub-limit on cyber extortion.

Is cyber insurance mandatory in Australia?

No, there is no general legal requirement for Australian businesses to hold cyber insurance. However, larger clients, government contracts, and regulated industries (healthcare, financial services) increasingly require evidence of cyber cover as part of vendor onboarding. The combination of the Privacy Act 1988 and the Notifiable Data Breaches Scheme means uninsured businesses carry the cost of every breach personally.

What is the difference between first-party and third-party cyber cover?

First-party cover pays for damage to your own business, such as data recovery, business interruption, and incident response costs. Third-party cover pays for damage to others caused by an incident at your business, such as customer compensation, legal defence, and regulatory defence. Most modern Australian cyber policies include both.

Does cyber insurance cover business email compromise (BEC)?

Most modern Australian cyber policies may cover BEC and funds transfer fraud, often as separate insuring sections with their own sub-limits, subject to policy terms. Cover may depend on the specific facts of the incident, including whether the business followed its own verification procedures. Always check the policy wording for the relevant sub-limit and any required controls.

How quickly can I get cyber insurance through upcover?

Eligible Australian businesses can typically receive an online quote in minutes through upcover. Once a policy is confirmed and paid, a Certificate of Currency is issued instantly. For businesses with more complex risk profiles, the upcover team can arrange tailored cover from a panel of Australian and global cyber insurers.

The information in this article is general in nature and provided for informational purposes only. It does not constitute personal advice on the insurance products or coverage levels appropriate for your specific situation. The insurance information has been prepared without taking into account your individual needs, objectives, or financial situation. It should not be relied upon as personal advice. Scenarios described in this article are illustrative only and do not represent confirmed coverage outcomes. Coverage depends entirely on the terms, conditions, limits and exclusions of the individual policy. Always read the relevant Product Disclosure Statement before purchasing. Cost ranges are indicative, based on 2026 Australian commercial cyber insurance market data, and are not a quote or guarantee of premium. All insurance products arranged through upcover are subject to the terms, conditions, limits and exclusions contained in the relevant policy wording and Product Disclosure Statement. upcover Pty Ltd ABN 17 628 197 437 is a Corporate Authorised Representative (CAR 1299211) of Experience Insurance Services Pty Ltd ABN 41 657 596 506, AFSL 539078. upcover arranges insurance products with selected insurers and underwriters and does not compare all general insurers or insurance products available in the market.

Mobile plant and equipment insurance may cover excavators, loaders and machinery against theft, fire, accidental damage and transit risks. See the guide.

We are digitising commercial insurance and risk management for small, mid-market and technology businesses. We work with a global network of underwriters, challenging legacy brokers and delivering market leading coverage to our customers.

The information contained on this website is general advice only and has been prepared without taking into account your individual needs, objectives and financial situation. It should not be relied upon as advice. All insurance products are subject to the terms, conditions, limits and exclusions contained in the relevant policy wording and Product Disclosure Statement. Before deciding whether a particular insurance product is right for you, please consider your personal circumstances and read the relevant Product Disclosure Statement, Target Market Determination, Policy Wording, and Financial Services Guide.

.svg)

.svg)

.svg)

.svg)

.svg)