Select how you’d like to proceed with your insurance needs.

Schedule a Call Today

Talk to a real insurance expert on your time.

BOOK A CONSULTATION

WHAT’S IN THIS STEP

15-minutes consultation with licensed advisors

Perfect if you’re unsure about coverage needs

Get personalised recommendations

Make upcover your insurance broker

Already have coverage? Let’s simplify your service

CHANGE BROKER

WHAT’S IN THIS STEP

Keep your current carriers & policies

Simple digital authorisation process

Seamless transition to better service

Business 101

When Should You Buy Business Insurance?

June 29, 2026

7 Mins Read

A small business should check business insurance before the risk starts. This may be before client work, contract commencement, site access, hiring staff, leasing premises, using vehicles, buying tools or stock, selling products, handling customer data, or taking on work that requires proof of insurance.

You may not need every type of cover while you are still planning. But once the business starts creating legal, contract, customer, asset, staff, vehicle, product, data or income risk, it is time to check what insurance may apply.

Adviser shortcut: If the business is still only planning, you may be able to wait. If money, clients, staff, vehicles, stock, tools, premises, customer data or contracts are involved, check cover before that activity starts.

Start With the Next Risk, Not Just the ABN

You may not need business insurance the day you register an ABN. In Australia, the better question is: what risk starts next? If you are about to work with clients, sign a lease, attend a site, hire staff, use a vehicle, buy stock, store customer data or show a Certificate of Currency, it is time to check cover. The simple rule is: Buy or check business insurance before the risk starts, not after something goes wrong.

Many businesses register an ABN before they trade. Some spend weeks or months planning, building a website, testing pricing or setting up systems before they take on real exposure. The trigger is usually not the ABN itself. The trigger is the first real business activity that could create financial loss, legal responsibility or a contract obligation.

In Australia, timing often comes down to workers compensation rules, CTP for registered vehicles, lease or contract requirements, and whether someone asks for a Certificate of Currency.

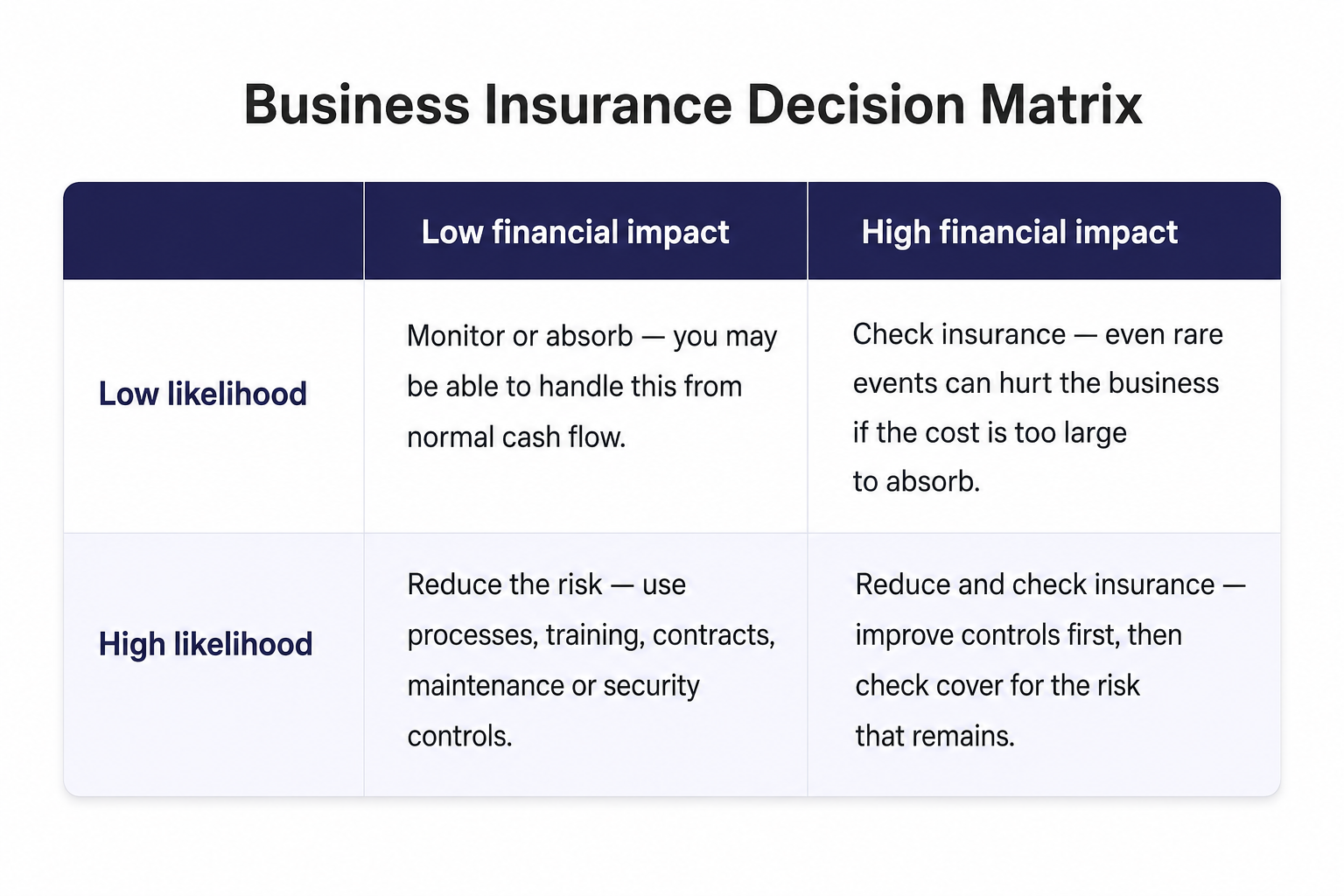

Simple Business Insurance Decision Matrix

Use this matrix to decide whether to wait, reduce the risk, or check insurance before the activity starts.

This is not a replacement for insurance advice. It is a simple way to think about timing. If a risk is high impact, legally required, contract-required, or too expensive to absorb, check cover before that activity starts.

Ask four questions:

Is it legally required? If yes, check cover before the legal obligation starts.

Is it required by a contract, lease, venue, platform or client? If yes, arrange the required cover before the relevant deadline, commencement date or site access date.

Could one event seriously affect cash flow? If yes, check whether insurance can help transfer part of that risk, subject to policy terms.

Can you reduce the risk yourself? Use controls first, such as safe work processes, contracts, cyber security, secure storage and staff training. Then check insurance for the risk you cannot comfortably absorb.

Insurance is not a substitute for good risk management. It is one part of the risk management plan.

9 Triggers To Look: When to Check Business Insurance

Use this as a quick scan. If one of these events is about to happen, check whether cover should be arranged before it starts.

Timing trigger

Cover to check

Why timing matters

Before starting client work

Public liability, professional indemnity

Clients may ask for proof before work starts

Before signing or starting a contract

Cover listed in the contract

Your Certificate of Currency may need to match the required cover and limit

Before signing a commercial lease or using premises

Public liability, business pack

Landlords may require proof before access, lease start or fit-out

Before hiring staff

Workers compensation

Workers compensation may be required if you employ staff

Before using vehicles for work

CTP, commercial motor, business-use vehicle cover

CTP generally does not cover vehicle damage or property damage

Before buying tools, stock or equipment

Tools cover, business pack, property cover

Assets can be stolen or damaged before revenue starts

Before selling, supplying or importing products

Products liability

Product-related claims can arise after goods reach customers

Before giving advice, treatment, designs or professional services

Professional indemnity

A client may allege your work caused financial loss

Before handling customer data or online payments

Cyber insurance

Cyber risk can start as soon as systems, invoices or customer data are active

This table is a starting point only. The right timing depends on your business activities, contracts, legal obligations, insurer appetite and policy wording.

Trigger 1: Before Starting Client Work

Check insurance before client work starts, especially if the client asks for proof of cover or your work could affect another person, property, finances, data or business outcome.

Public liability may be relevant if you visit sites, meet customers or deal with the public. Professional indemnity may be relevant if you provide advice, reports, services, care, treatment, recommendations or designs. If you already know you need cover, see how to buy small business insurance online.

Trigger 2: Before Signing or Starting a Contract

Check the insurance clause before signing or starting work. Some contracts require cover from the signing date. Others require it before work starts, site access, onboarding or a specific commencement date.

Look closely at:

required policy type;

required cover limit;

insured entity name;

policy period;

Certificate of Currency requirements.

If your Certificate of Currency does not match the contract, the client may ask you to fix it before work can continue.

Trigger 3: Before Signing a Lease or Using Premises

Check cover before lease commencement, fit-out, stock delivery or customer access. Many commercial landlords may require public liability before a lease starts. Business pack cover may also be worth checking if you have stock, contents, fit-out, glass, equipment or business interruption exposure.

This can apply to shops, cafes, clinics, salons, offices, warehouses, studios and shared commercial spaces.

Trigger 4: Before Hiring Staff

Check workers compensation before workers start. Workers compensation may be required if you employ staff. Rules differ by state and territory, and some schemes may treat certain contractors differently depending on the work arrangement.

Check motor cover before using a vehicle for business. CTP or third-party personal injury insurance is required for registered vehicles. But CTP generally does not cover vehicle damage, third-party property damage, tools, stock or goods in the vehicle.

Personal car insurance may also exclude or limit business use. Commercial motor may be relevant for deliveries, trades, mobile services, client visits, transporting tools, transporting goods, staff driving or regular business travel.

Trigger 6: Before Buying Tools, Stock or Equipment

Check cover before valuable assets are purchased, delivered, stored or transported.

Risk does not wait until the first sale. A tradie may need tools cover before storing tools in a vehicle. A retailer may need stock cover before inventory arrives. A cafe may need business pack cover before fit-out and contents are installed. An ecommerce business may need marine cargo before imported goods are shipped.

Trigger 7: Before Selling, Supplying or Importing Products

Check products liability before goods reach customers. Product-related claims can arise after a product leaves your business. This may matter for ecommerce stores, retailers, food businesses, importers, wholesalers, market stalls, beauty brands and manufacturers.

Trigger 8: Before Giving Advice, Services, Designs or Treatment

Check professional indemnity before delivering advice, services, care, treatment, reports, recommendations or designs. This may matter for consultants, IT contractors, designers, engineers, bookkeepers, allied health professionals, NDIS providers, support businesses and other service providers.

Trigger 9: Before Handling Customer Data or Online Payments

Check cyber insurance before customer data, online payments, cloud systems or email invoicing become active. Cyber risk can start early. A small business may be exposed through email compromise, invoice fraud, ransomware, customer data, booking systems, payment systems or cloud software.

The right timing depends on what stage your business is in. A market stall, sole trader, ecommerce store, startup and larger business may all hit the same triggers at different times.

Idea or Pre-Launch Stage

You may not need every cover while you are only planning, researching or setting up admin. But check insurance if you are already signing contracts, buying valuable tools or stock, leasing premises, hiring staff, testing services with real clients, collecting customer data or taking deposits.

If the business is still only an idea, insurance may not be urgent yet. If the business starts creating obligations or exposure, the timing changes.

First Client or First Paid Job

Check insurance before the work starts. This is usually the first real risk point for consultants, trades, freelancers, support workers, designers, online service providers and other sole traders.

Market Stall, Event or Pop-Up Stage

Check insurance before the event, market or venue date. Market organisers, councils, venues and event operators may ask for a Certificate of Currency before approving your stall, site or attendance. If proof of insurance is required, arrange it before the organiser’s deadline.

Online Business or Ecommerce Stage

Check cover before taking orders, importing stock or storing customer data. An online business may still have real-world risk. Products can injure customers. Stock can be stolen or damaged. Customer data can be exposed. Email invoices can be intercepted.

Tradie, Mobile Service or Site-Work Stage

Check cover before attending site, storing tools or using vehicles for work. Trades, installers, technicians, cleaners, mobile beauty services and other site-based businesses often need proof of insurance before site access or contractor onboarding.

Hiring Stage

Check workers compensation before workers start. This may apply when you hire full-time, part-time or casual staff, and some contractor arrangements may also need review depending on state or territory rules.

Growth Stage

Review insurance when the business changes. Growth does not only mean more revenue. It can mean new services, bigger contracts, more assets, staff, vehicles, premises, customer data or legal obligations.

If you move from sole trader to company, check that the insured name, ABN or ACN, trading name and Certificate of Currency match the entity doing the work. A mismatch can create problems at claim time or when a client checks your documents.

Larger Business or Enterprise Contract Stage

Check insurance before tendering, onboarding or starting work. Larger clients, government tenders and enterprise vendor systems may require specific cover types, higher limits, Certificates of Currency, policy wording or endorsements.

At this stage, insurance is not only risk protection. It can become a business access requirement.

When Should Existing Businesses Review Insurance?

Review business insurance when the business changes. This is especially important when the change affects your declared business activities, insured entity, cover limits, locations, staff, assets or contracts.

Review cover when you:

add new services;

change the way work is performed;

increase revenue;

hire staff;

buy tools, stock, vehicles or equipment;

move premises;

start selling products;

store more customer data;

sign larger contracts;

work interstate or overseas;

change from sole trader to company;

add directors, investors or a board;

receive new contract insurance requirements.

Also watch for scope creep. Do not assume your old policy automatically follows you into a new kind of work. For example, a domestic cleaner who adds high-pressure roof cleaning, solar panel cleaning or working at heights has changed the risk profile of the business. A consultant who starts giving regulated advice, handling client funds or building software may also change their risk profile.

If your policy only describes the old activity, it may not match the new work. Update your declared business activities before relying on the policy for the expanded service.

What Happens If You Wait Too Long Before Buying Business Insurance?

Waiting too long can create practical and financial problems.

You may face:

client onboarding delays;

rejected or delayed site access;

lease or venue conditions not being met;

stock, tools or premises being uninsured;

workers compensation obligations being missed;

a vehicle policy that does not match business use;

a Certificate of Currency that lists the wrong entity;

a claim connected to work done before cover started.

Insurance is usually arranged before the risk starts. It is not something to organise after a claim, accident, theft, cyber incident or contract issue has already happened.

How upcover Can Help You With Business Insurance

upcover helps Australian small businesses arrange insurance online with selected insurers and underwriters. Cover options depend on your occupation, business details, insurer appetite, policy terms and underwriting requirements. Depending on your occupation and eligibility, upcover can help you:

get quotes online for eligible business types;

access AI-powered instant quoting where available;

review cover options from selected insurers and underwriting partners;

receive a Certificate of Currency on policy confirmation where available;

access monthly payment options where available;

access digital claims lodgement support where available;

get support if your business activities or contract requirements need clarification.

upcover is rated 4.9+ for customer experience and is designed to make business insurance simpler, faster and easier to manage online.

A small business should check insurance before the risk starts. This may be before client work, contracts, leases, staff, vehicles, tools, stock, products, customer data, site access or proof-of-insurance requirements.

Do I need business insurance before registering an ABN?

Not always. Registering an ABN alone may not create the same risk as trading, signing contracts, hiring staff, buying assets or working with clients. Check insurance once real business activity or obligations begin.

Do I need insurance before starting work with a client?

If the client requires insurance, arrange the required cover before the work starts. They may ask for a Certificate of Currency as proof.

Do I need insurance before signing a lease?

Many commercial landlords may require public liability before a lease starts. You may also want to check business pack cover if you have stock, contents, fit-out or equipment.

Do I need insurance before hiring employees?

Workers compensation may be required if you employ staff. Check your state or territory rules before the worker starts.

Can I buy insurance after winning a contract?

You may be able to buy insurance after winning a contract, but before starting the work. Check the contract carefully because it may require proof of cover before commencement, site access or the date the agreement is signed.

Does business insurance cover past work?

It depends on the policy type and wording. Some policies, such as professional indemnity, may depend on claims-made wording, retroactive dates and continuous cover. Check the policy wording before relying on cover for prior work.

When should I review business insurance?

Review insurance cover when your business changes, including new staff, services, premises, vehicles, stock, products, revenue, client contracts, data exposure, business structure or insured entity.

What is the difference between when to buy and how to buy business insurance?

“When to buy” is about timing. It helps you work out the business trigger that makes insurance worth checking. “How to buy” is about the quote process, including what details to prepare, how to compare quotes and how to get a Certificate of Currency.

The information in this article is general in nature and provided for informational purposes only. It does not constitute personal insurance, legal, financial, tax or business advice. It does not take into account your objectives, financial situation or needs. Insurance requirements vary by occupation, industry, state, territory, licence, contract and business circumstances. Cover depends on the policy wording, limits, exclusions and insurer appetite. Before purchasing or relying on an insurance product, consider the relevant Product Disclosure Statement, Target Market Determination, Policy Wording and Financial Services Guide. upcover Pty Ltd ABN 17 628 197 437 is a Corporate Authorised Representative (CAR 1299211) of Experience Insurance Services Pty Ltd ABN 41 657 596 506, AFSL 539078. upcover arranges insurance products with selected insurers and underwriters and does not compare all general insurers or insurance products available in the market.

Opening a business in Australia? See what insurance to check before signing a lease, hiring staff, buying stock, using vehicles, taking payments or starting work.

Learn when small businesses may need insurance, including before client work, contracts, leases, staff, vehicles, stock, products, data or business growth.

We are digitising commercial insurance and risk management for small, mid-market and technology businesses. We work with a global network of underwriters, challenging legacy brokers and delivering market leading coverage to our customers.

The information contained on this website is general advice only and has been prepared without taking into account your individual needs, objectives and financial situation. It should not be relied upon as advice. All insurance products are subject to the terms, conditions, limits and exclusions contained in the relevant policy wording and Product Disclosure Statement. Before deciding whether a particular insurance product is right for you, please consider your personal circumstances and read the relevant Product Disclosure Statement, Target Market Determination, Policy Wording, and Financial Services Guide.

.svg)

.svg)

.svg)

.svg)

.svg)