Select how you’d like to proceed with your insurance needs.

Schedule a Call Today

Talk to a real insurance expert on your time.

BOOK A CONSULTATION

WHAT’S IN THIS STEP

15-minutes consultation with licensed advisors

Perfect if you’re unsure about coverage needs

Get personalised recommendations

Make upcover your insurance broker

Already have coverage? Let’s simplify your service

CHANGE BROKER

WHAT’S IN THIS STEP

Keep your current carriers & policies

Simple digital authorisation process

Seamless transition to better service

Insurance Basics

Professional Indemnity vs Public Liability Insurance: Do You Need Both?

June 26, 2026

5 Mins Read

Professional indemnity and public liability insurance cover different risks. Public liability may help cover claims where your business activities cause third-party injury or property damage. Professional indemnity may help cover claims that your professional advice, service, mistake, or omission caused a client financial loss. They are not interchangeable, and many Australian businesses that provide services or advice while also interacting with clients, sites, or property may need both.

The simplest way to think about it: public liability is mainly about physical risk. Professional indemnity is mainly about advice and service risk. This guide explains the difference and helps you work out whether you need one, the other, or both.

At a Glance

Public liability generally responds to third-party injury or property damage from your business activities.

Professional indemnity generally responds to financial loss claims from advice, services, mistakes, or omissions.

Businesses that provide advice or services AND interact with clients in person may need both.

PI is often written on a claims-made basis. PL is commonly occurrence-based. These work differently, so switching insurers or retiring requires extra care with PI.

Neither policy is designed to cover your own injury, employee injuries, tools, cyber incidents, motor accidents, or management decisions.

If you sell or supply physical products, check whether products liability is included in your PL policy.

How Professional Indemnity and Public Liability Compare

Public Liability

Professional Indemnity

What risk does it cover?

Third-party injury or property damage

Client financial loss from advice or service errors

Typical claim trigger

Someone is hurt or something is damaged because of your business activities

A client alleges your advice, service, or omission caused them a loss

Example

A customer trips in your office and breaks their wrist

A client loses money after relying on your financial forecast

Policy basis

Often occurrence-based

Often claims-made

Who commonly arranges it

Trades, retailers, venues, service businesses

Consultants, accountants, designers, allied health, IT

Often required by

Landlords, venues, councils, head contractors

Regulators, professional bodies, client contracts

Covers your own injury?

No

No

Covers employees?

No (workers' compensation)

No (workers' compensation)

Public liability may also bundle products liability, which covers claims from products you sell or supply. For more, see upcover's guide on what is public liability insurance.

Professional indemnity may respond to allegations of negligence, mistakes, omissions, breach of duty, breach of confidentiality, or lost documents, depending on the policy wording. For some occupations, PI may also respond to claims connected to professional treatment or services. It may include legal defence and investigation costs, depending on the policy wording. For more, see upcover's professional indemnity insurance guide.

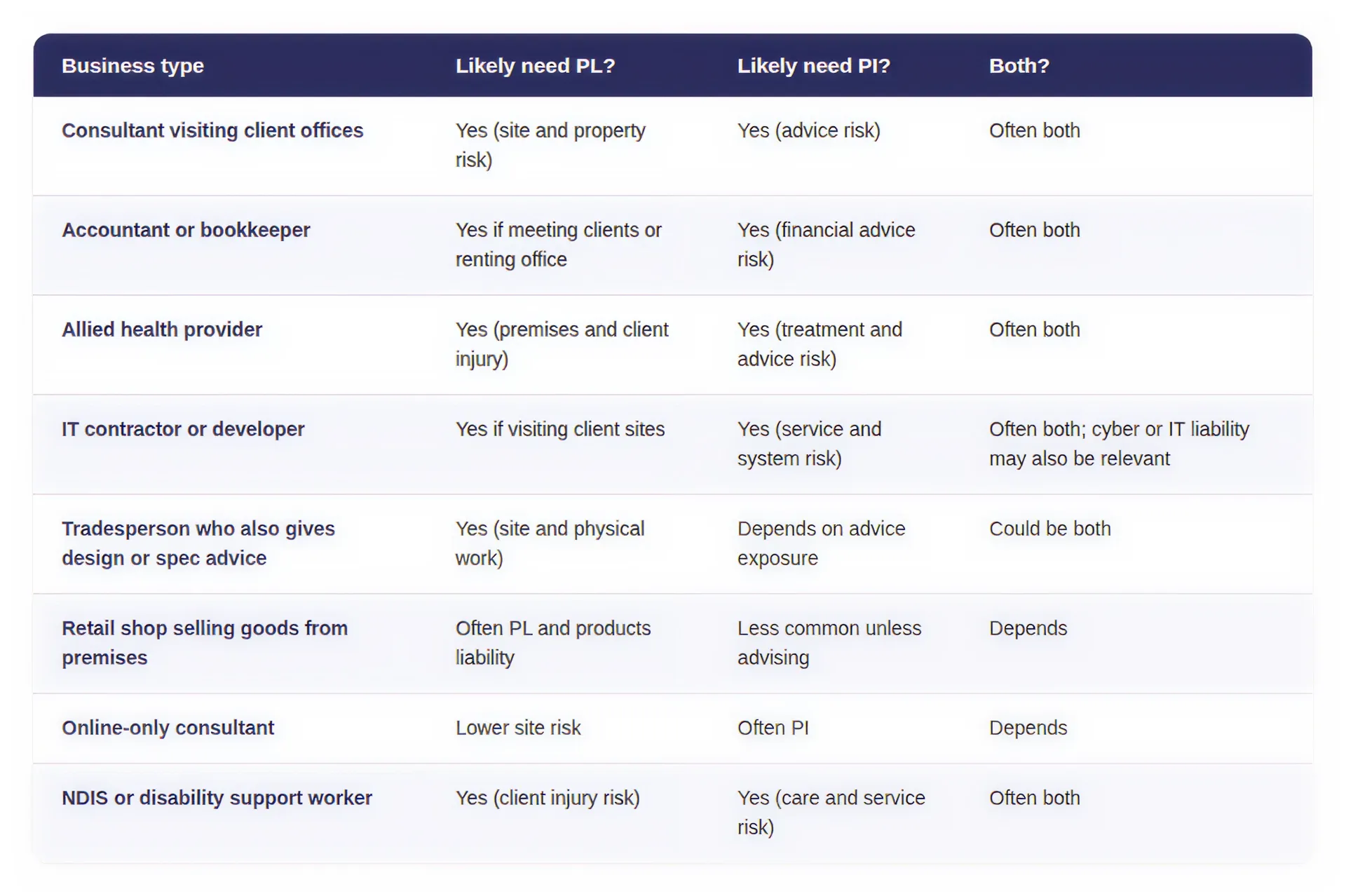

Public Liability only may be enough if your main risk is third-party injury or property damage and you do not provide advice or professional services. A retailer, market stallholder, or cleaner who does not give professional recommendations may fall into this group.

Professional Indemnity only may be enough if your main risk is advice or service error and you have limited physical interaction with clients or property. A remote bookkeeper or software developer who never visits client sites may fall here.

Both are worth considering if you provide advice or services AND meet clients, visit sites, operate from premises, or handle client property. Contract, licence, or professional body requirements may also require both regardless of your risk profile.

Real Claims: Would PI or PL Respond?

Client trips over your bag in their office. A consultant visits a client and leaves a laptop bag in the walkway. The client trips and fractures their wrist. PL may respond, subject to policy terms.

Incorrect report causes client financial loss. An accountant prepares a financial forecast with errors. The client relies on it, makes a business decision, and suffers a loss. PI may respond, subject to policy terms.

The designer damages client property during a site visit. While inspecting a home, an interior designer accidentally knocks over an expensive vase. PL may respond, subject to policy terms.

Allied health treatment allegedly worsens a condition. A therapist recommends a treatment plan the client alleges was unsuitable. Their condition worsens. PI may respond, subject to policy terms.

Some incidents may involve elements of both physical damage and professional service issues. Which policy responds depends on the facts and the insurer's assessment. Illustrative scenarios only. Coverage depends on the specific facts, policy wording, terms, and exclusions.

What Professional Indemnity and Public Liability Do Not Cover

Neither policy is a catch-all. Other risks need their own cover:

Intentional misconduct or fraud is usually excluded under both policies.

Can You Get Professional Indemnity and Public Liability in One Policy?

Some businesses buy PI and PL as separate policies. Others may be able to get both in a package, depending on the occupation and insurer.

Allied health providers, care and support workers, consultants, IT professionals, and professional services businesses often quote both together. Not every occupation can get bundled cover, so check with your broker or insurer what options are available.

What to Check Before You Buy

Before arranging cover, work through these questions:

Are all your services and occupations correctly listed on the policy?

Do your contracts require PI, PL, or both, and at what limits?

Is PI written on a claims-made basis, and what retroactive date applies?

Are prior claims or known circumstances disclosed?

Are subcontractors covered or excluded?

Does PL include products liability if you sell or supply goods?

Are cyber, IT, privacy, or data risks handled separately?

Can you get a Certificate of Currency showing the correct covers?

How upcover Can Help

upcover arranges professional indemnity and public and products liability insurance for eligible Australian businesses with selected insurers and underwriters. Depending on your occupation and insurer, you may be able to quote online, bind cover, and access a Certificate of Currency.

70,000+ businesses covered across Australia.

4.9/5 customer rating.

Instant Certificate of Currency on policy confirmation.

upcover Pty Ltd ABN 17 628 197 437 is a Corporate Authorised Representative (CAR 1299211) of Experience Insurance Services Pty Ltd ABN 41 657 596 506, AFSL 539078.

FAQ

What is the difference between professional indemnity and public liability insurance?

Public liability may help cover claims where your business activities cause third-party injury or property damage. Professional indemnity may help cover claims that your advice, service, mistake, or omission caused a client financial loss. PL is mainly about physical risk. PI is mainly about advice and service risk.

Do I need both professional indemnity and public liability insurance?

It depends on your business. If you provide advice or professional services AND interact with clients, visit sites, or operate from premises, you may need both. Check your contracts, professional body requirements, and insurer options.

Is professional indemnity the same as public liability?

No. They cover different risks and respond to different types of claims. A client tripping in your office is usually a PL claim. A client alleging your advice cost them money is usually a PI claim.

Does public liability cover professional advice?

Generally no. PL covers third-party injury and property damage, not financial loss from advice. If a client alleges your advice caused them a financial loss, that is usually a PI claim.

Does professional indemnity cover injury or property damage?

PI is generally designed for claims arising from professional advice or services, which typically involve financial loss. For some occupations, PI may also respond to claims connected to professional treatment or service where injury is alleged. Public liability is usually the more relevant cover for third-party injury or property damage. The distinction depends on the policy wording and facts.

Which insurance do consultants need?

Many consultants consider both PI (for advice and service risk) and PL (for client site visits, meetings, and premises risk). Some client contracts specify minimum PI and/or PL limits. For more, see who needs professional indemnity insurance.

Can I buy PI and PL together?

Some insurers and brokers offer PI and PL as a package depending on your occupation. Allied health, care workers, consultants, and professional services businesses often quote both together. Not every occupation can get bundled cover.

Is professional indemnity insurance claims-made?

Most PI policies in Australia are written on a claims-made and notified basis. The policy in force when the claim is made or notified responds, not the policy in force when the incident happened. This makes the retroactive date and run-off cover important if you switch insurers or retire.

Can a claim involve both public liability and professional indemnity?

Yes. Some incidents may involve both physical damage and professional service issues. For example, a design error may lead to property damage, or a service failure may cause both rectification costs and third-party loss. Which policy responds depends on the facts, policy wording, exclusions, and the insurer's assessment.

Written by upcover's editorial team. Reviewed for insurance content accuracy. The information in this article is general in nature and provided for informational purposes only. It does not constitute personal insurance, legal, or financial advice. It does not take into account your objectives, financial situation, or needs. Whether you need professional indemnity, public liability, or both depends on your occupation, contracts, professional body requirements, and policy wording. Before purchasing or relying on an insurance product, consider the relevant PDS, Target Market Determination, policy wording, and Financial Services Guide. upcover Pty Ltd ABN 17 628 197 437 is a Corporate Authorised Representative (CAR 1299211) of Experience Insurance Services Pty Ltd ABN 41 657 596 506, AFSL 539078. upcover arranges insurance products with selected insurers and underwriters and does not compare all general insurers or insurance products available in the market.

Reiki practitioners are commonly offered combined liability, meaning professional indemnity and public liability in one policy, with products liability where they sell oils, crystals or other items.

We are digitising commercial insurance and risk management for small, mid-market and technology businesses. We work with a global network of underwriters, challenging legacy brokers and delivering market leading coverage to our customers.

The information contained on this website is general advice only and has been prepared without taking into account your individual needs, objectives and financial situation. It should not be relied upon as advice. All insurance products are subject to the terms, conditions, limits and exclusions contained in the relevant policy wording and Product Disclosure Statement. Before deciding whether a particular insurance product is right for you, please consider your personal circumstances and read the relevant Product Disclosure Statement, Target Market Determination, Policy Wording, and Financial Services Guide.

.svg)

.svg)

.svg)

.svg)

.svg)